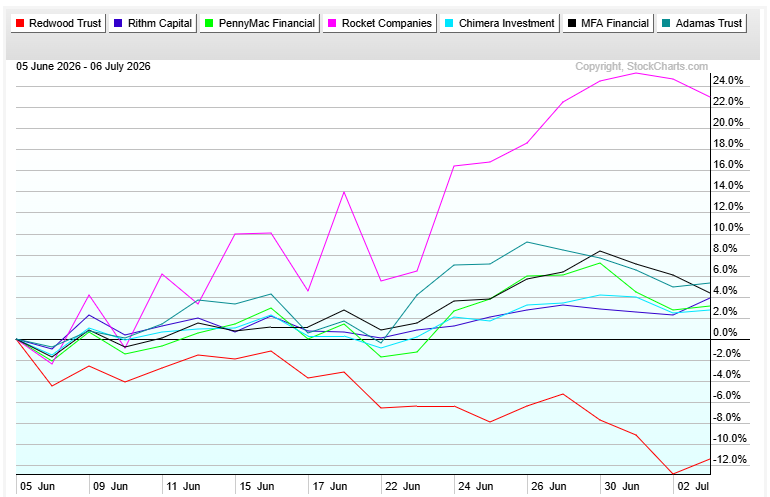

Redwood Trust: Mortgage Banking Platform Depressed by Index Deletion

Ejection from the S&P600 Small Cap index effective July 8 has created an opportunity to buy Redwood Trust (RWT) at a deeply discounted valuation when its operating business has never been more attractive:

Transformation into a platform for third party capital investments through blue chip partnerships (Silverlake, CPP, and Oaktree)

Strong market share in core residential mortgage products (Jumbo residential mortgages, Alt-A, and Business Purpose Lending)

BVPS $7.12 as of 3/31/26 (est $6.98 for 2Q26)

2026 Analyst Consensus Earnings Available for Distribution $1.03/share

Topics:

Index Deletion - the near-term opportunity

Segments - background on RWT’s business

Balance Sheet Risk - high headline leverage

Distributions - tax advantaged 16% yield

Breaking: RWT estimated a 1-3% decline in 2Q26 BVPS (LINK). This does not change the thesis of this article.

Index Deletion

S&P announced on July 2 that RWT would be removed from the S&P600 on July 8. Approximately $135Bn is directly indexed to the S&P600 and at a 0.03% weighting, that means approximately 4mm shares of RWT. Volume in the past week has probably been sufficient to clear this.

No peer has the same business mix as RWT, but share prices of every company that competes with part of RWT’s business are flat or up in the past month.

RWT’s exchange traded bonds and preferred shares are all up slightly over the past month, showing no sign of company specific problems.

Segments

Redwood purchases loans from banks and other originators then securities them or sells in bulk. In 1Q26 it saw record production volume of $8.5Bn and issued 11 securitizations despite relatively weak housing market conditions. Financial performance is detailed in the quarterly supplement.

Sequoia - Prime Jumbo Loans. RWT has been in this business for 30 years, has approximately a 7% market share, and estimates that it works with loan sellers and banks responsible for 45% of all originations. Loans underlying $21Bn of Sequoia securitizations have an average FICO of 772 and 0.2% 90+ delinquency. At 3/31/26 RWT had $230mm of capital invested in Sequoia retained interests and $500mm of working capital invested in current loan production.

Corevest - Investor Loans. RWT formed this segment in 2019 with the acquisition of Colony American Finance. It makes Residential Transition Loans and DSCR-based loans for stabilized properties. Loans underlying $1.9Bn of Corevest securitizations have an average 9.8% 90+ delinquency. At 3/31/26 RWT had $92mm of capital invested in Corevest retained interests and $174mm of working capital invested in current loan production.

Aspire - non QM loans (Alt-A). In 2025 RWT began leveraging its Sequoia seller relationships to develop an “expanded-prime” platform supporting loans based on wealth or self-employment income. Loans have an average FICO of 754 and 70% LTV. At 3/31/26 RWT had $200mm invested in working capital to support Aspire current loan production.

Investments - Retained Interests. RWT retains equity interests in securitizations. It also holds third-party originated MSRs. Results from this segment include fair value changes that are the primary difference between RWT’s GAAP income and non-GAAP “Earnings Available for Distribution”.

Legacy. In 2025 RWT began segregating assets not aligned with its high volume core business. These included multifamily, home equity, and re-performing loans. Low turnover, higher credit losses, and negative carry made these a drag on earnings. At 3/31/26 RWT had $242mm of capital invested in legacy assets (-54% yoy). As these are wound down, the funds are being re-allocated to the higher RIE core businesses.

The high ROE from the mortgage banking business (60% for Sequoia in 1Q26 😲), strong market presence including relationships with loan sellers and securities investors, and blue-chip capital partnerships make RWT fundamentally different from a traditional mortgage REIT that simply owns a highly leveraged investment portfolio. Focus on its core business lines and successful reallocation of capital from legacy assets could justify a valuation at a premium to book value ($7.12/share)

Partnerships

RWT has transformed its business in recent years through formation of joint ventures to invest in the assets created under the Redwood platform. These partnerships enable to RWT to increase volume-based earnings by expanding the scale of its of its business while also earning management and incentive fees (terms are not disclosed)

2023 Oaktree - In June 2023 RWT formed a $1Bn venture with Oaktree for investment in Corevest business purpose loans (LINK)

2024 Canada Pension Plan - In March 2024 RWT formed a $4Bn venture to invest in Corevest loans. CPP contributed $400mm of equity and a $250mm secured credit line. (LINK)

2026 Castlelake - In April 2026 RWT formed an $8Bn venture to invest in Sequoia prime jumbo loans. (LINK)

Balance Sheet Risk

RWT’s balance sheet is complex with $890mm of common equity supporting $26,816mm of total assets. However $22,076mm of the assets are in consolidated securitization trusts with permanent non-recourse financing. A majority of the remaining assets are current loan production financed with warehouse lines until securitization. RWT also has $777mm of unsecured corporate debt (including several exchange traded bond issues).

RWT has transformed its liability structure since 2020 when it faced severe pressure from excessive reliance on marginable financing. At 12/31/19 RWT had $1,177mm of repo financing for its retained securities. Deleveraging and mark-to-market changes resulted in a $582mm ($5.12/share) loss for 2020. At 3/31/26 RWT had only $104mm of marginable financing for its retained securities so it will be more resilient if a crisis emerges.

Distributions

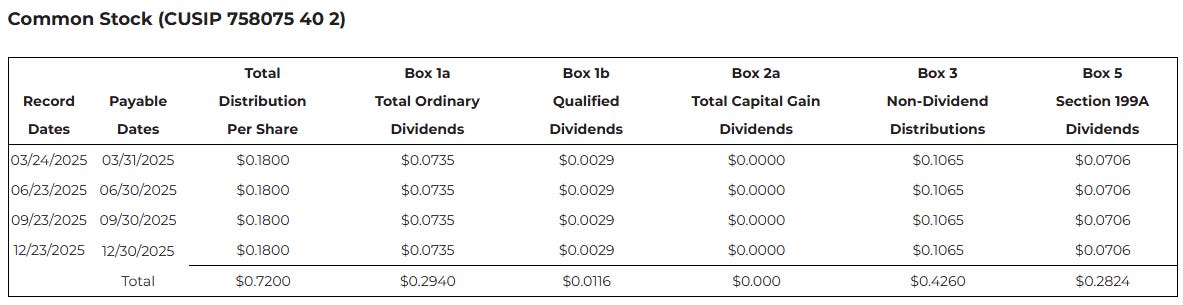

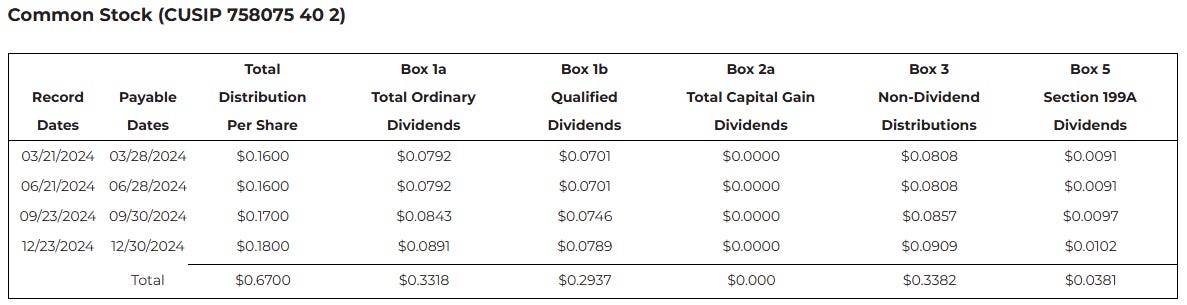

RWT is a Mortgage REIT with a current quarterly dividend of $0.18/share that is covered by non-GAAP Earnings Available for Distribution ($0.21/share in 1Q26). While the current yield of 16% suggests a high risk level, that’s attributable to the share price discount. The distribution is about 10% of book value, well below the ROE of each core segment. The payout ratio is declining due to a favorable earnings trend from strong mortgage banking volume, capital from new partnerships, and recycling of capital from legacy assets. There is no risk of a distribution cut in the near-term and the dividend returns a portion of the full NAV that we can currently buy in the market at a large discount.

The 2020 losses created loss carryforwards that have shielded a portion of the tax liability on current distributions. 59% of 2025 dividends and 50% of 2024 dividends were non-taxable return of capital.

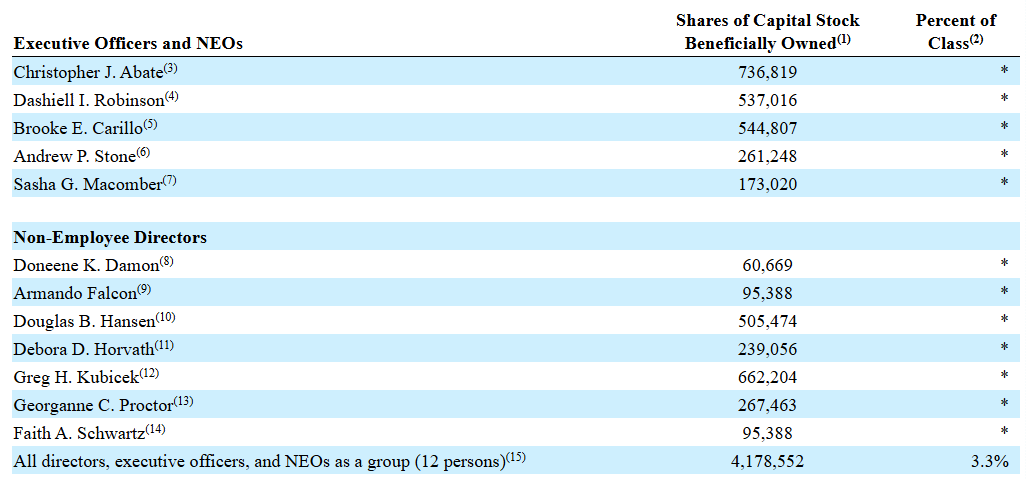

Governance

RWT has over a 30-year history as a public company

Insider ownership is low and over 50% in the form of incentive Deferred Stock Units rather than common shares.

Institutional Ownership is passive and traditional investors

Blue chip partnerships are a validation of the quality of management and internal controls

Disclosures and Notes:

At the time of publication the author held shares of Redwood Trust. This disclosure should not be interpreted as a recommendation to purchase this security and this holding may change at any time. Investors are encouraged to check all of the key facts cited here from SEC filings, company disclosures, and other sources prior to making any investment decisions. The author believes all information in the article is accurate as of the date of publication.

This article is published free in its entirety because it does not contain a lot of original work.