Canadian Real Estate 04/24/26

M&A Perspectives and Some Trade Ideas Updates

Canadian Real Estate has begun 2026 with a +9.1% total return (XRE a/o 4/24). US REITs are +8.3%, and the CAD is +0.4% vs USD.

Real estate fundamentals have been favorable with strong demand, limited supply, and improved credit availability in most segments. But it’s hard to assess valuation and outlook with an uncertain macro outlook:

Iran conflict is severely impacting global supplies of critical commodities (oil, LNG, refined products, fertilizer, aluminum, helium, sulphur and more). Arjun Murti says extended closure of the Strait of Hormuz could have an economic impact worse than the 2008 financial crisis and a humanitarian impact worse than COVID. Bad! I think it’s politically impossible for Trump to resume an aggressive bombing campaign or to seize Iranian territory with ground forces, but the diplomatic path to peace is unclear.

Trade conflict may return to the headlines in coming months. Most Canadian exports to the US are not subject to tariffs as a result of the CUSMA agreement signed with the Trump administration in 2020. Each party has an option to decline renewal of the agreement in July 2026, however that only leads to a mandatory annual review process to try to resolve differences. Even in the absence of resolution, the agreement would not end until 2036. Each party also has the option to withdraw completely from the agreement with six month’s notice. The Canadian government is approaching this summer’s deadline as a “checkpoint, not a cliff”. Trump is unlikely to reciprocate in that orderly approach and may try to create a crisis.

As an exporter of energy and food, Canada benefits in some ways from high prices resulting from Strait of Hormuz closure. The war has also made the US more dependent on imports of Canadian aluminum in spite of tariffs.

Topics

M&A Perspective ($) Thoughts following the First Capital takeover.

Office ($) Strong leasing and weak unit/share prices. Comments on Allied and Dream Office.

Industrial ($) Comments on Dream Industrial and Nexus

Residential ($) Is this the bottom for Toronto multifamily? Comparison of 2025 SPNOI growth among North American REITs. Comments on Morguard Residential and GO.

Retail ($) Comparison of 2025 SPNOI growth among Canadian REITs. Comments on Primaris.

Diversified ($) Comments and H&R and Morguard REIT.

REOCs ($) Comments on Dream Unlimited and Melcor Developments.

Other ($) Comments on Dream Impact and Ravelin.

Sector Overview

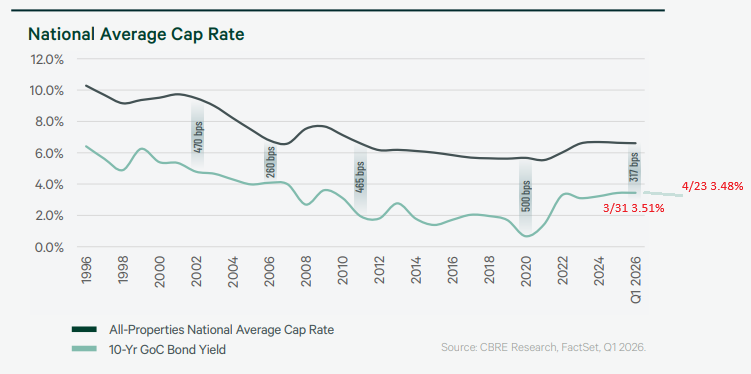

The yield premium of real estate cap rates over 10-year bond yields is near the middle of its historical range. Rates are close to unchanged since 3/31, but credit spreads for REIT debentures have narrowed a bit.

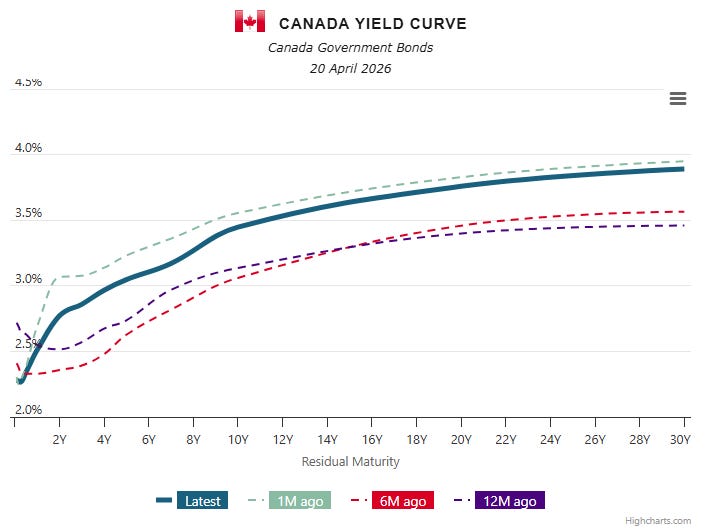

Most of the Canadian yield curve has moved higher over the past year due to expectations for improved growth and higher inflation. That environment would benefit more economically sensitive properties such as Industrial and Retail. Higher rates are a challenge for low yielding Multifamily assets.

Insiders at 20 of 38 REIT/REOCs were buyers since 1/1/26 and 7 had net insider sales. REIT/REOCs have repurchased $264mm of equity since 1/1 (reported to 4/24) with the largest buybacks at Dream Industrial (2.4% of market cap), Boardwalk (1.9%), Dream Unlimited (0.9%), and Riocan (0.8%).