Rithm Property Trust: Massive Value Transfer To External Manager Through Heavily Dilutive Financing

Rithm Pooperty (RPT) shares are -18% since announcing a heavily dilutive $300mm equity offering and -62% since announcing in 2024 that Rithm Capital would become its external manager.

Key aspects of the financing:

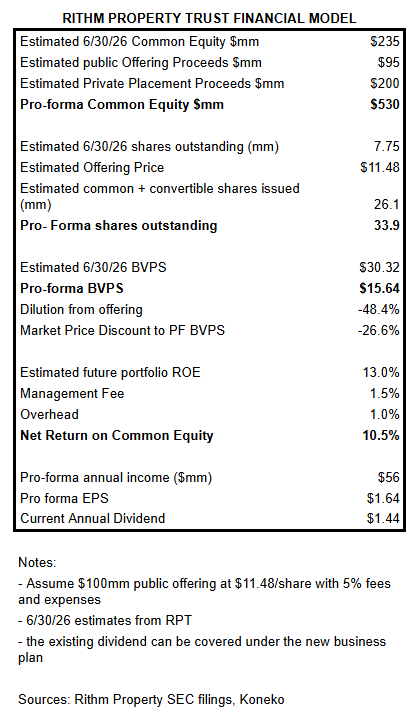

Approximately 48% dilutive to Book Value per share

Rithm Capital will invest up to $200mm in the financing (prospectus) through a combination of common shares (up to the maximum 20% of voting power permitted under NYSE regs) and non-voting convertible preferred that are substantially equivalent to common shares.

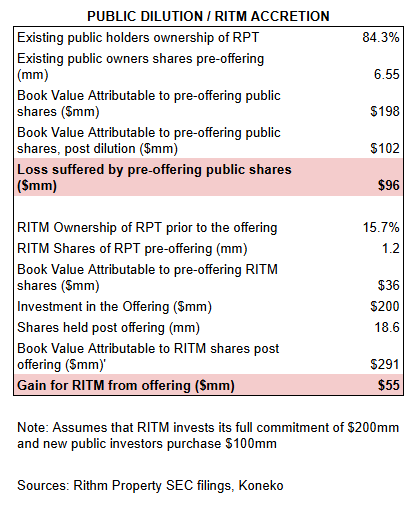

Existing holders other than Rithm Capital will suffer a loss of $96mm from dilution of their current interest in RPT’s book value. A holder could mitigate the impact by purchasing shares in the offering. If RITM purchases $200mm of new equity then it could gain $55mm in attributable book value.

Proceeds will be used to acquire a $1Bn portfolio of multifamily transition loans (construction, bridge, and renovation) from Rithm Capital’s Genesis division. The portfolio has an estimated levered yield of 13.4%.

The Genesis portfolio might be attractive, however it could never deliver enough gains to offset the huge upfront loss in value from the offering. On the other hand, the deal looks extremely attractive for Rithm Capital which will grow the fee paying AUM of RPT, have a captive vehicle to hold its Genesis loan production, and profit through the dilution of public RPT holders.

Shame on the purportedly independent directors of RPT for approving this equity issuance. Rithm Capital has delivered an excellent long-term return to its own shareholders. Unfortunately, this is a bad deal for RPT. It should be abandoned, but that probably will not happen.

Meet The Bagmakers

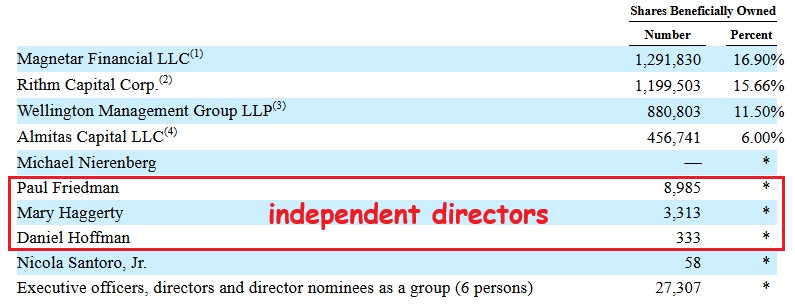

RPT’s three independent directors are bagmakers, not bagholders. The recent annual meeting signaled a high level of opposition, however the 4 nominees receiving the most votes serve on the board regardless of the number of votes against them.

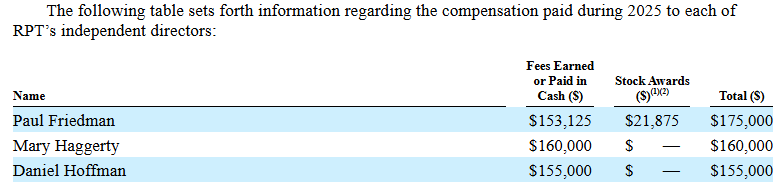

The directors receive generous annual cash compensation:

They hold little or no RPT stock and all reported shares were received as compensation rather than purchased in the market.

Share price performance during their terms of service has been terrible:

Paul Friedman joined the Board of RPT predecessor Great Ajax in July 2016 with the share price at $83.28 (pre-consolidation). RPT claims that he has “extensive amount of operational and risk management experience to the Board, as well as a deep knowledge of the financial services industry.” He is also on the board of Oppenheimer Holdings.

Mary Haggerty joined the Board of RPT predecessor Great Ajax in March 2021 with the share price at $70.80 (pre-consolidation). RPT claims that her “background in investment banking paired with her experience in various director roles provide her with the expertise to serve as a director.”

Daniel Hoffman joined the RPT board in June 2024 with the share price at $19.68. RPT claims that his “over 25 years of experience in the mortgage securities market and his broad-based investment banking experience qualify him to serve as a director.” He also serves as CEO of The Monday Group family office (“Compounding intelligence - Amplifying curiosity”).

Disclosures & Notes

At the time of publication the author held shares of Rithm Capital and Rithm Property Trust. This disclosure should not be interpreted as a recommendation to purchase either security. These holdings vary in size and may change at any time. Investors are encouraged to check all of the key facts cited here from SEC filings, company disclosures, and other sources prior to making any investment decisions. The author believes all information in the article is accurate as of the date of publication.

This article is published free in its entirety because it may be of public interest.