Cresud: Long-Term Value Compounder Faces Near-Term Challenge From High Fertlizer Prices

Shares of Argentine real-estate business Cresud (NASDAQ:CRESY) have recently been weak due to the anticipated impact of soaring prices for imported fertilizer resulting from the Iran War. Cresud will be directly affected in its farmland operations (soy, corn, and cattle) and indirectly as the impact on the national economy will harm the company’s urban commercial real estate (shopping malls, offices, and residential development).

Cresud’s financial reporting reflects variable weather conditions, commodity prices, and land sales that can obscure the company’s multi-year value creation. If the share price responds negatively to comments about the near-term outlook in the 5/7 earnings release and 5/8 conference call then it would be a great opportunity for long-term investors.

Topics:

Iran War impacts - fertilizer prices soaring and inventories critically low

Argentina Economy and Milei Impact - strong rebound

Argentina’s Economic And Political Cycles

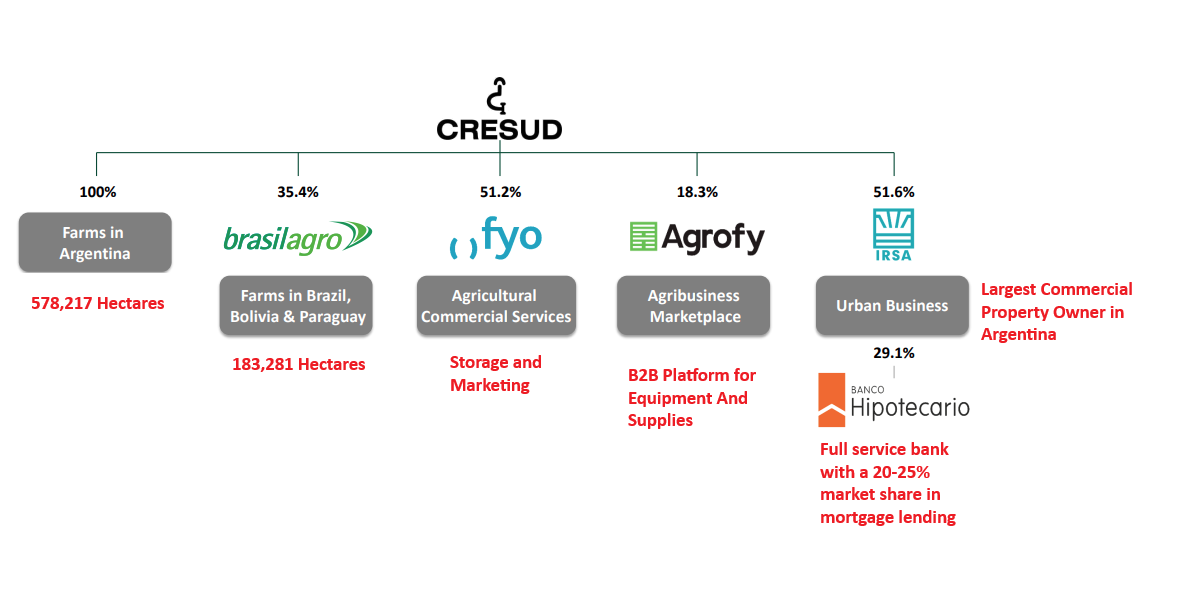

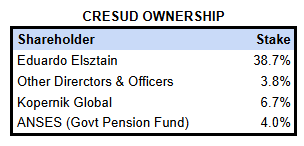

Cresud Corporate Structure and Governance - Insiders own 42.5% of Cresud and Cresud owns 51.6% of IRSA

Cresud Dividends - substantial, but variable payments

Cresud Farm Business ($) Value creation through cyclical landbanking, land upgrading, land sales, and farm operations

Cresud Commercial Real Estate ($) Value creation through ownership and development

Cresud Valuation ($) +90% increase in NAV per share over the past 5 years

Cresud Risks & Catalysts ($)

The Iran War

Argentina is a exporter of many commodities (metals, energy, grains, lithium and more) so it could be a long-term beneficiary of Middle East insecurity, but the near-term impact is mostly negative.

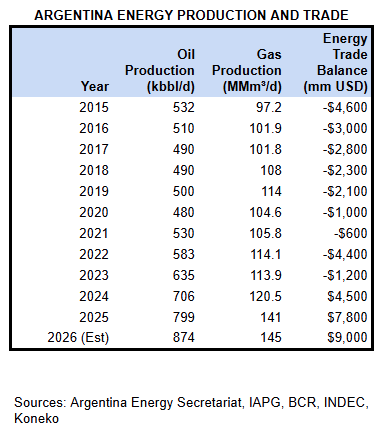

Development of the Vaca Muerta shale oil field over the past 5 year has made Argentina a significant oil exporter. In contrast to past cycles, the country is now self-sufficient in oil, natural gas, refined products (diesel, gasoline, jet fuel). Significant hard currency export revenues support the balance of payments and international reserve position.

However other sectors are dependent on imports affected by the Strait of Homuz closure:

Argentina imports 65% of its fertilizer, and nitrogen is sourced primarily from the Middle East. Urea prices jumped 54% in March and retail prices in some areas rose even more. Inventories are critically low right ahead of the Southern Hemisphere summer planting season. Farmers are responding by shifting acreage from corn to soybeans and sunflower (less nitrogen intensive), and limiting fertilizer to their most productive land. While corn and soybean prices are higher, increased shipping costs have pressured ex-farm prices. Producers like Cresud may report increased top line revenues, but margins will be the smallest in years. Agriculture and related services account for about 23% of the national economy.

Fuel prices may add 1% to annual inflation even though state-controlled YPF has cushioned part of the retail impact.

The ARS exchange rate has a controlled depreciation based on the inflation rate - higher inflation will result in currency depreciation.

Argentina Economy and Milei Impact

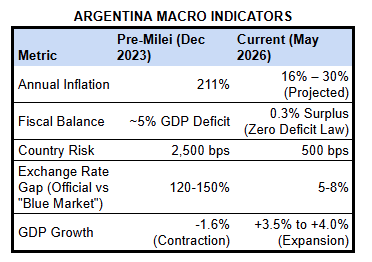

Shock therapy has been incredibly successful.

Stabilization of the exchange rate and protections for foreign investments (RIGI) that guarantee 30-year tax and legal stability have resulted in a surge of foreign investment in mining and infrastructure (pipelines, ports, and data centers). The RIGI was structured with layers of protection that could not quickly be unwound by a new government (“Acquired Rights” after 40% of capital has been committed, international arbitration, international treaty commitment, and provincial commitments mirroring RIGI). Annual foreign capital investment in Argentina has increased from about $11Bn in 2020-2022 to about $30Bn forecast for 2026.

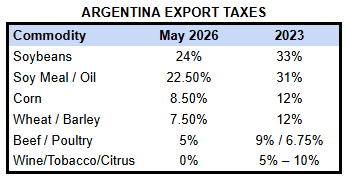

The farm sector environment has significantly improved:

Export taxes have been reduced by about 1/3

Export sales revenues converted at the official exchange rate now receive close to fair value in pesos.

Milei opponents argue that the standard of living for ordinary people has suffered as reduced pensions and removal of subsidies for energy and utilities has squeezed affordability of food, housing etc.. The next national election is not until October 2027, but Milei’s reforms will be more sustainable if they are codified through legislation passed this year.

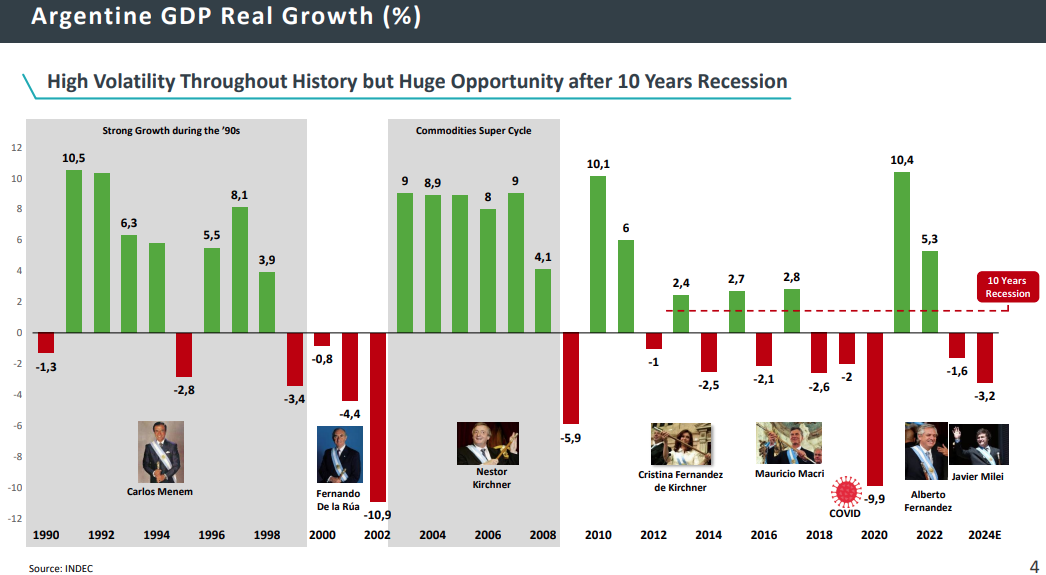

Argentina’s Economic And Political Cycles

Cresud’s 2024 Roadshow nicely documented Argentina’s cyclical history. The country enjoyed strong growth, stable currency, and a primary fiscal surplus during the 1990s and then during the 2003-2007 commodity boom.

Cresud’s share price has shown similar volatility.

Ironically, the sharp share price decline from 2017-2019 resulted from failed attempts to diversify the business outside of Latin America.

IRSA suffered cumulative losses of over US$850mm on investments in highly leveraged Israeli conglomerates IDB Development and Discount Investment Corporation. They ultimately went bankrupt in 2000 under COVID stress.

IRSA lost over US$40mm on its investment through a consortium that purchased the “Lipstick Building” in Manhattan in 2008 and then surrendered it to the ground lessor in 2020.

IRSA lost approximately US$19mm through an investment in Condor Hospitality (originally Super-tel) that began in 2012 and ended when Condor was acquired by Blackstone in 2021.

If Cresud and IRSA had limited themselves to their core business in Argentina then they would have recorded impressive value creation despite the difficult macro environment from 2012-2022.

Corporate Structure and Governance

Cresud is Argentina’s leading real estate company with the largest farm acreage, largest commercial property GLA, and stakes in complimentary service companies.

Eduardo Elzstain has held a controlling stake and been Cresud Chairman since 1994. His brother Alejandro is CEO. The Board of Directors includes Eduardo Elsztain’s wife, cousin, and two sons. Outside influence is limited.

Alejandro Elsztain recently purchased 17,833 ADS. It only increased his holding by 1.5% so perhaps he wanted to send a signal of confidence in the company amid market uncertainty.

Eduardo Elsztain has investments outside of Cresud/IRSA, including several in Argentina’s mining sector (Austral Gold and Argenta Silver), but I am not aware of any that compete with Cresud or create any potential conflict of interest.

In my opinion, Cresud has treated public shareholders conscientiously. Shareholder communications are excellent with quarterly earnings calls, informative presentations, and occasional investor roadshows. I enjoyed a helpful conversation with Alejandro Elsztain in New York in 2024.

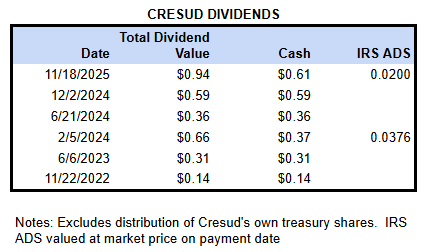

Most importantly, Cresud pays meaningful dividends that deliver a portion of the value it creates each year.

Dividend History

Due to capital controls, Cresud has been paying dividends to ADS holders using a mixture of cash and IRSA ADS.

The irregular timing and mixed consideration results in some information services not correctly recognizing them. Full details are on the Cresud news page.