Clarke Inc: Value Compounder Just Acquired a Distressed REIT

Canadian activist investor George Armoyan’s Clarke Inc (TSX:CKI) tripled its assets by acquisition of Ravelin Properties through a discounted debt exchange. Clarke will recognize an immediate bargain purchase gain of approximately $94mm ($5.77/share). This article will consider potential further upside and the pro-forma valuation of Clarke’s shares.

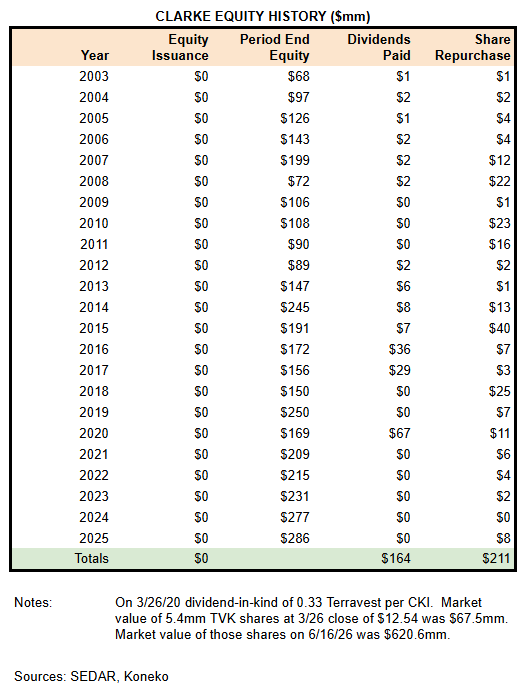

Since Armoyan became CEO of Clarke Inc in April 2003, investors have enjoyed an IRR of approximately 15% assuming reinvestment of dividends (Clarke calculates an IRR of 11.7% excluding reinvestment). Shareholders’ Equity is +320% and shares outstanding are -51%. The return would be even higher if credit were given for appreciation of Terravest shares since they were distributed to CKI holders in March 2020. Armoyan’s stake has risen from 26% in 2003 to 73% as a result of open market purchases, plus reduction of the public float through NCIB and SIBs.

Armoyan’s willingness to issue CKI shares for the first time in 23 years suggests he must believe strongly in the value that will be realized over time through the Ravelin acquisition.

Topics:

Armoyan’s involvement with Ravelin

Clarke’s History of Value Creation

Armco and G2S2

Ravelin’s History of Value Destruction

Pro-Forma Financials

Summary Of Investment Opinion ($)

Clarke Business Profile Post-Merger ($)

Clarke Valuation ($)

Armoyan’s Involvement With Ravelin

Armoyan first reported ownership of 10.1% of Ravelin (f/k/a Slate Office) in May 2022. Based on market prices at that time over $4.50, the position must have cost over $36mm. Subsequently:

Over the next year he purchased an additional 6.5mm units at a cost of approximately $20mm. He liquidated his entire holding in December 2025 for less than $5mm.

In February 2023 a settlement agreement added Armoyan and a chosen nominee to the Slate Office board.

In November 2024 Armoyan became board Chairman and the management agreement with Slate was terminated. The REIT was renamed Ravelin Properties.

In 2025 Armoyan, through G2S2, acquired C$724mm of defaulted Ravelin debt and provided a brief period of forbearance during which the REIT could develop a restructuring plan.

In March 2026 Ravelin announced an agreement to be acquired by Clarke and the transaction closed in May. Each Ravelin common unit was exchanged for 0.000582 shares of CKI (value about C$0.015/unit) and Ravelin convertible debentures were exchanged for Clarke shares worth approximately 36% of principal.

The discounted exchange value of $158mm of debentures is responsible for the estimated $94mm bargain purchase gain that Clarke will record from the merger.

Clarke’s History Of Value Creation

Milestones:

1921 Clarke Steamship Company founded. By 2000 it was a “transportation and logistics solutions company”.

2002 Armoyan (through Geosam) acquired a stake of 20% in Clarke Inc and took over as CEO in February 2003.

By 2006 CKI described itself as an “activist catalyst investor”. Significant transactions:

2003 Concord Transportation sold to ATS and equity was monetized in 2005

2004 Logistics division sold to PBB Global

2004 Acquired 50% interest in 8 warehouses

2006 Financial statements began to include an “Investment” segment. The segment reported gains in 2006 and 2007 and then a very large loss in 2008. Fortunately, it had no long-term debt due until 2012. BVPS did not recover to its 2007 peak until 2013. Individual investments mentioned over time include Versacold, Advanced Fiber Technologies, “Energy Basket”, Avenex, Bonnett’s Energy, Royal Host, Supremex, Vitran, Highkelly Energy, Imvescor Restaurant, Sherritt, Keck Seng, and Trican.

2008 acquired Home Heating Business

2014 Sold remaining Transportation business

2014 Acquired 35% of Holloway Lodging

2016 Raised stake in Terravest to 31%. The shares were distributed to CKI shareholders in March 2020 when their value during COVID stress was $58mm

2019 Acquired remaining shares of Holloway in September 2019 - unfortunate timing just before COVID

2019 Acquired 3 vacant Houston office buildings far below their replacement cost. They were sold in 2023-24 farther below their replacement cost.

2021 Began building a residential tower in Ottawa.

2023 CKI began describing itself as an “Investment and Real Estate Company”.

2025 CKI described itself as a “Real Estate Company with holdings across real estate sectors – primarily residential, furnished suites and hospitality”. The latest:

The broad investment themes were distressed income trusts in the 2000s, distressed energy in the 2010s, and perhaps distressed real estate in the 2020s.

Armco and G2S2

George Armoyan has a history of additional real estate investments through his private entities:

Armco Capital became the largest residential land development company in Halifax in the 1980-90s through countercyclical acquisitions of landbank followed by entitlement, servicing, and sale to builders (similar to the Western Canada land businesses of Melcor and Dream). In the past few years it has made large acquisitions of Calgary office properties (First Canadian Centre, Bow Valley Square and others).

G2S2 primarily makes public equity investments. It acquired over 10% of Cominar REIT in 2020 and sold at a $100mm profit to the Artis consortium in 2022. Armoyan was lucky because Artis overpaid and ultimately lost its entire investment in the buyout. G2S2 has invested over $100mm in Morguard Corporation and $50mm in Morguard REIT. And G2S2 spent over $50mm acquiring 18% of Ravelin/Slate Office - nearly all lost. Outside of real estate, G2S2 has held stakes in Calfrac, Western Energy Services, Tourmaline Oil, Nixon Energy, and Knight Therapeutics.

Ravelin’s History of Value Destruction

Ravelin operated until 2024 as Slate Office REIT (SOT.UN) under external control by Slate Asset Management. The REIT focused on “workplace real estate” in suburban and secondary markets. Higher-yielding non-prime properties, high leverage, and high payout ratio supported a high distribution rate that attracted investors to 4 secondary offerings, ATM issuance, and 2 convertible bond sales. Proceeds financed growth in assets from $271mm at 12/31/14 to $1,869mm at 12/31/22. External asset management fees grew from $0.7mm in 2013 to $5.8mm in 2022.. Armoyan estimated that including fees for property management and transactions, Slate Asset Management earned over $132mm from Slate Office. Book Value per unit dropped from $11.05 at 12/31/13 to ($0.36) at 03/31/26.

The Slate legacy is a portfolio with no great assets. Armoyan’s business grew out of Atlantic Canada so he undoubtedly knows the region well, but even there, Slate focused on smaller markets of Fredericton, Moncton, and St Johns. In 2021 Slate acquired an Irish REIT (Yew Grove) at an valuation of C$255mm, calling it a "transformational jumping-off point" for further expansion in Europe. Armoyan strongly criticized the acquisition as dilutive to Slate’s reported NAV of $8.71. George seems to have put too much faith in the baggy “NAV discount” thesis.

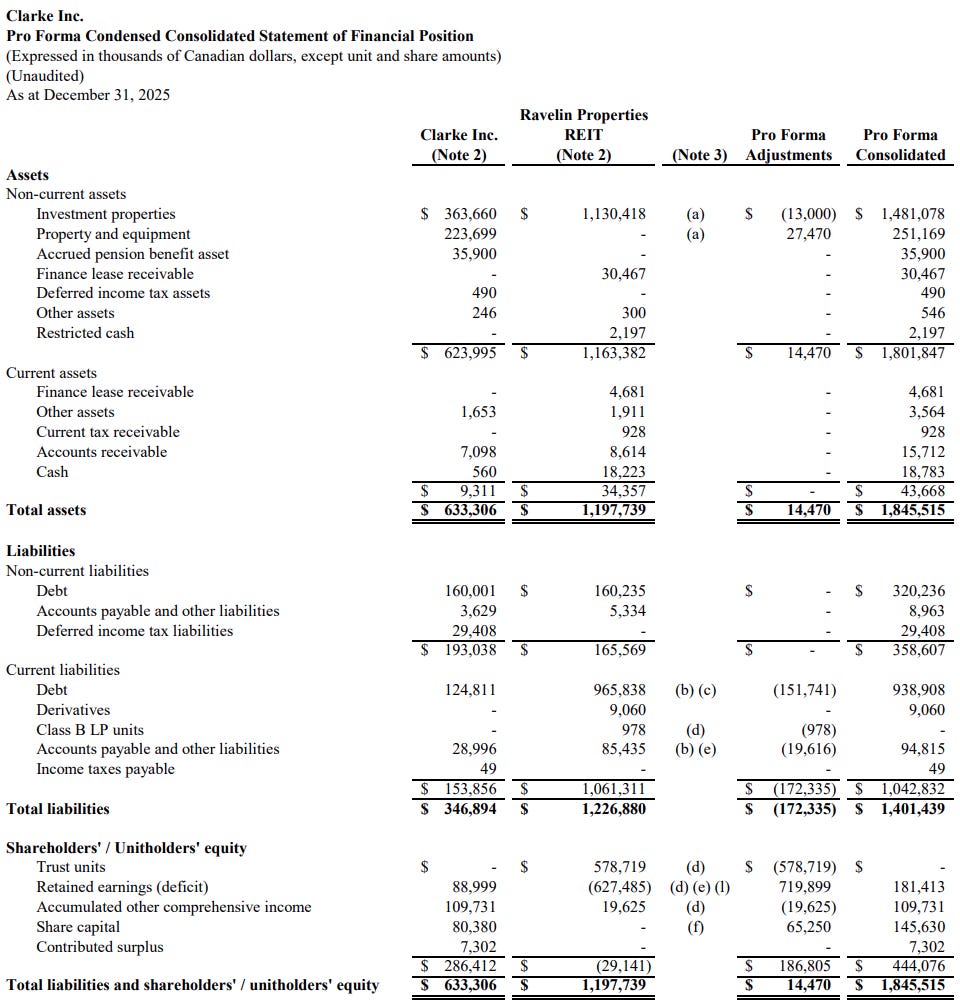

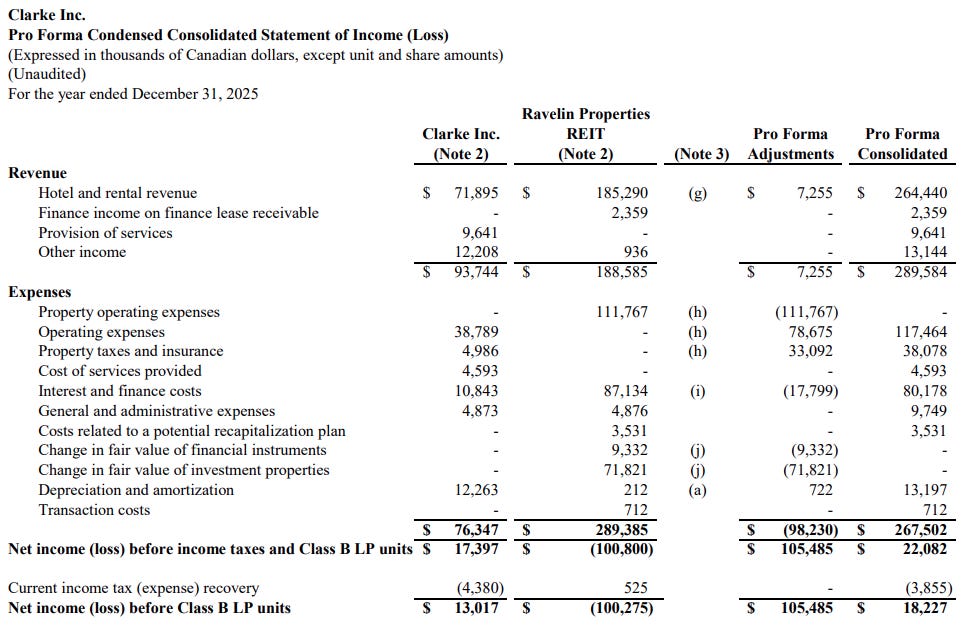

Clarke Pro-Forma Financials

Ravelin’s circular for its acquisition by Clarke included pro-forma financial statements as of 12/31/25. Key points:

The combined entity is very highly leveraged (debt/assets = 69%). Approximately $724mm of debt acquired through Ravelin is owed to G2S2.

Cash Flow (net income + depreciation + planning and transaction costs) would have been $39mm for the combined entities.